Why we built pfolio—and why DIY investing might be right for you

Let us be honest: the idea of DIY investing can feel daunting. Time-consuming. Complicated. More than a little scary. What if we told you it does not have to be that way?

At its core, managing your own investments is a skill that more people can—and we argue, should—develop. In fact, we have made it our mission to make that a reality.

Our mission

While it is true that access to financial markets has never been easier, with a universe of low-cost ETFs at our fingertips, the perceived friction remains high for many retail investors.

A case for DIY investing

But why consider DIY investing in the first place? Surely banks, mutual funds, and robo-advisors are doing a perfectly fine job—so why not just sit back and relax? And it is true: hands-off investing is certainly better than not investing at all.

But for anyone who is not afraid to open a brokerage account and buy or sell a few ETFs or stocks on their own, DIY investing can offer meaningful advantages for long-term success.

We have grouped these benefits into four categories—largely distinct, with some overlap.

Benefits of DIY investing

Lower fees

Harry Markowitz, Nobel laureate & founder of Modern Portfolio Theory, once said:

“Diversification is the only free lunch in investing”

There may be a corollary: minimising fees is the simplest way to avoid having that lunch eaten. While diversification builds your portfolio, fees quietly consume it.

For the DIY investor, this begins by forgoing the annual management fees that funds and robo-advisors charge on your total invested capital—a direct and perpetual drag that erodes compounding growth.

The long-term impact of a seemingly benign 1% annual management fee is staggering. Yet, many investors still pay this rate for actively managed mutual funds, or between 0.25% and 0.50% per year for a robo-advisor.

Impact of fees on investment performance

For perspective, a USD 10,000 investment in the S&P-500 over 40 years would incur total fees equivalent to 11 times the initial investment at a 1% annual fee.

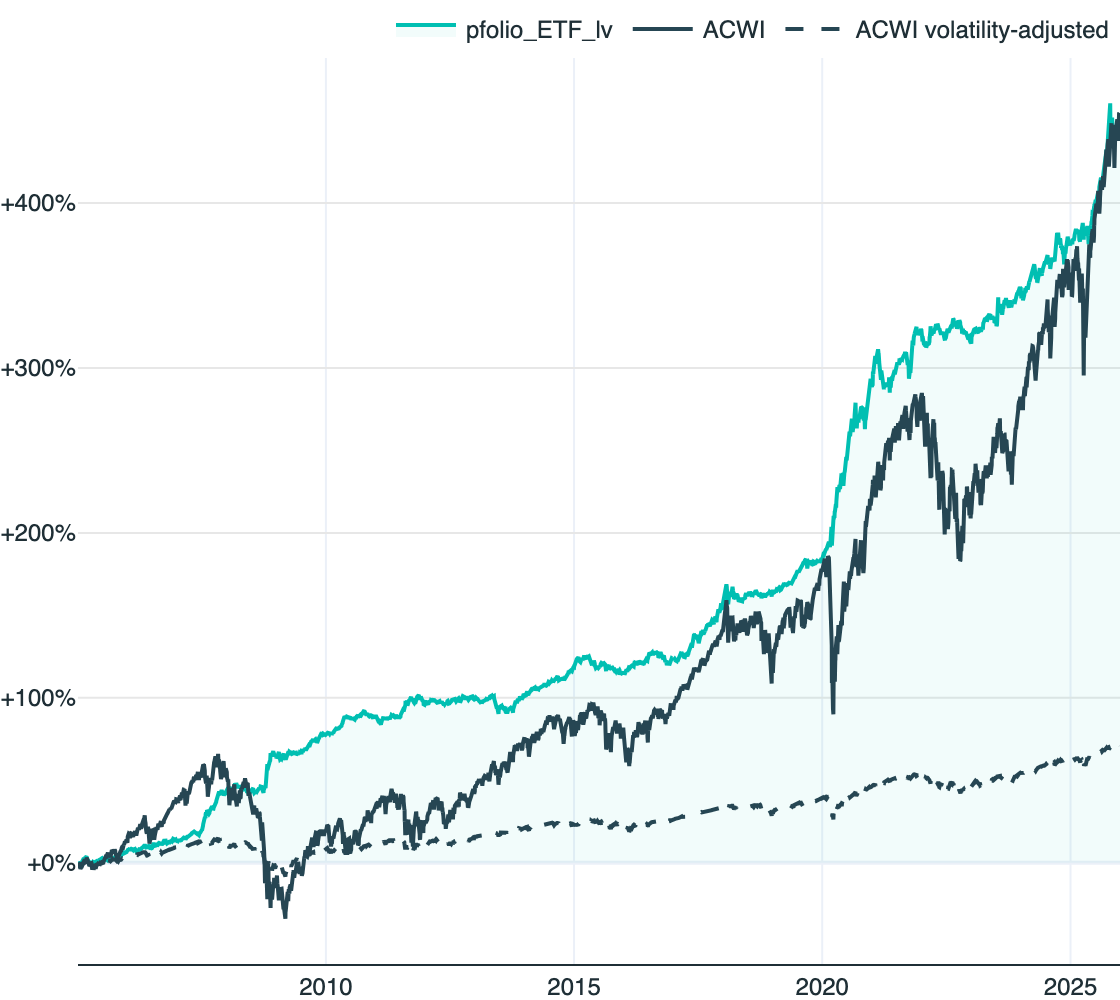

You can calculate this effect for any scenario using pfolio's Asset Builder.

Financial market efficiencies

Beyond lower fees, DIY investing provides direct levers to capture financial market efficiencies that are often automated away—or monetised—by managed platforms. For the informed investor, these efficiencies compound into significant long-term advantages.

While many nuanced tactics exist, from optimising deposit insurance to executing precise tax strategies, these two specific examples help demonstrate this broad potential.

Cash management

Traditional banks typically pay minimal to no interest on idle deposits. In contrast, most retail brokerages pay rates much closer to the prevailing benchmark interest rate, albeit often minus a modest spread.

on USD cash at major banks vs. major broker (2024)")

Interest (p.a.) on USD cash at major banks vs. major broker (2024)

The data from 2024—a period of higher interest rates—highlights this persistent gap: even in favourable rate environments, banks are often reluctant to pass on yields to retail clients.

To improve even further, DIY investors can opt for short-term government bonds or dedicated money market funds, which can offer higher yields while maintaining liquidity and capital preservation.

FX management

Many non-US investors accessing US markets face a critical choice: whether to accept or hedge the inherent currency risk. DIY investors have the granular control to make this decision strategically.

For example, a Swiss investor seeking exposure to the S&P-500 has several distinct implementation paths:

- Accept full FX risk: Convert CHF to USD and purchase a USD-denominated S&P-500 ETF. The entire investment principal and its returns are exposed to USD/CHF fluctuations.

- Actively hedge FX risk: Use a margin loan to borrow USD and purchase the ETF, simultaneously earning interest on CHF collateral and paying interest on the USD loan.

- Minimise FX risk: Purchase S&P-500 Index futures (e.g., ES contracts). This method requires only a margin deposit in CHF. The primary FX exposure is limited to the daily settlement of profits and losses, not the entire notional value of the exposure. Efficient USD financing is embedded in the futures price, making this a capital-efficient structure.

Complete control

Through DIY investing, investors retain complete control of their strategic and tactical investment decisions.

Asset selection

This includes the granular selection of assets. Investors can build portfolios that reflect personal criteria, such as ethical exclusions (e.g., no defence stocks) or tactical tilts (e.g., increased exposure to emerging markets).

Order execution

This control encompasses order execution, granting you direct authority over the timing, price, and method of every trade. You can execute orders at your chosen time, use limit orders to target specific entry points, and potentially earn liquidity rebates that can turn trading costs into a net credit.

Furthermore, you retain the ability to exit positions immediately—a critical feature for risk management, with near-24/7 availability for instruments like futures.

Platform independence

Finally, this autonomy extends to platform independence. Your assets remain fully portable, allowing you to transfer them between brokers without liquidation, thereby avoiding vendor lock-in and preserving continuous market exposure.

Financial literacy

DIY investing fosters financial literacy through direct experience. The process of researching assets, executing trades, and managing a portfolio provides irreplaceable insight into how markets function and how you react to volatility.

This self-knowledge and market understanding become foundational assets themselves, leading to greater confidence, discipline, and improved investment decision-making over time.

Missing tools for efficient DIY investing

It is easier than ever to become a DIY investor: access to retail brokers is simple, low-cost ETFs are plentiful, and quality educational content is widely available.

Yet, upon starting our investing journey, we realised that many critical decisions—both macro and micro—are specific to our case and can ideally only be answered in a systematic, data-driven way.

For example:

- What specific assets or ETFs should I select to build a properly diversified global portfolio?

- How do I determine the optimal asset allocation across stocks, bonds, and other asset classes?

- Should I hedge my foreign currency exposure, and if so, is it better to do so manually or by using a currency-hedged ETF?

- Does Bitcoin warrant a place in a diversified portfolio, given its high correlation with equities?

Answering these questions in depth is often complicated and time-consuming—beyond the scope of a simple spreadsheet or intuition.

Data can be scattered and methodologies unclear (how do you calculate a Sharpe ratio again?). We realised the core tools for efficient, data-driven DIY investing were missing.

So, we began building them ourselves. The result is pfolio—DIY investing without the downsides.

Disclaimer

Get started now